Landlords and renters’ insurance are different, in that landlords’ insure the building whereas renters insure their possessions within the building.

If your landlord has provided any furniture or items to make your home more comfortable like a sofa, bed frame, fridge-freezer, or microwave, these will need to be covered by their own content insurance.

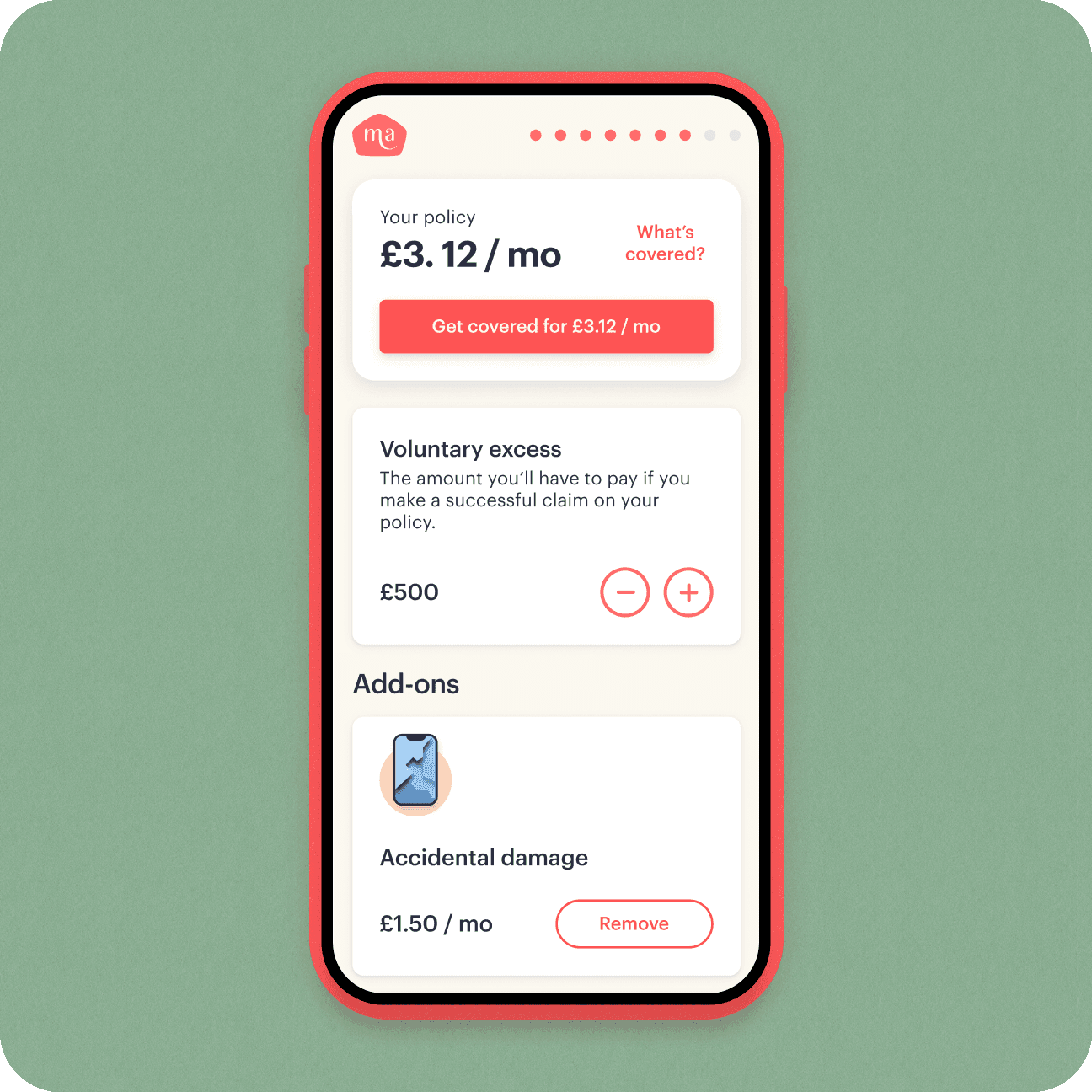

So that they can claim for any accidental theft or damage to their possessions, landlords who offer furnished or part-furnished rentals usually make the decision to take out contents insurance to protect the items in the home that belong to them and aren’t covered by buildings insurance.

And that’s sensible because while you as the tenant live in the house, their contents are subject to any unforeseen events and accidents too.

This means that as a tenant, you’ll need to take out your own contents insurance so you can make a claim if anything within the property that belongs to you is damaged or stolen.

And likewise, you can’t see an accident coming. You won’t know that a fire will start, or a water leak could spring up which damages everything in your living room. So, it’s a recommended course of action.

Neither party necessarily needs to take out contents insurance as there is no legal requirement to take out policies such as these, however it is in both of their best interests to do so.

Opting to go without contents insurance means that any damage or loss of belongings resulting from unfortunate incidents such as fires, theft, and vandalism will have to be repaired or replaced at the owner’s expense. And not everyone has a pot of cash at the ready for situations like this.