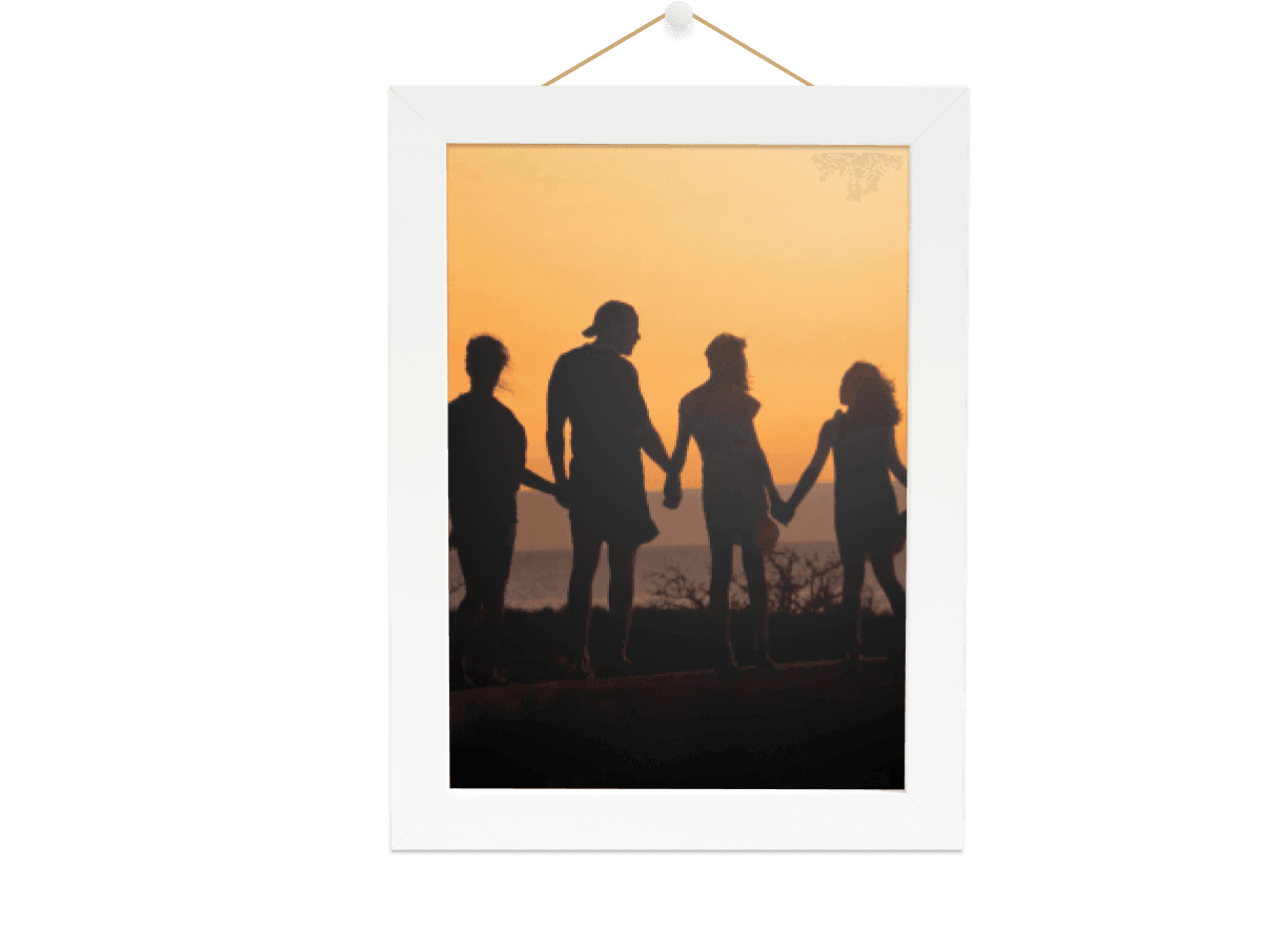

Having Life Insurance is not legally required to get a mortgage, however many lenders make it a precondition for their mortgages. Life Insurance not only protects your family in the future, but it protects the lender’s investment, so without Life Insurance, you may find it tricky to get a mortgage.

As landlords have more properties than residential homeowners, it makes sense that they would also need cover to protect their families in the event of death, by clearing outstanding mortgages and any other debts.